Indian B2C Digital business landscapehttps://qwixpert.com/wp-content/uploads/2023/07/Picture9-scaled.jpg25601707qwixpertadminqwixpertadminhttps://secure.gravatar.com/avatar/392f1042eaff5c1f343a179d15026010?s=96&d=mm&r=g

Digital in numbers, but not the numbers corporate India is used to seeing

In this day and age, yesteryear business metrics such as revenue growth or profit margins, cannot adequately summarize the nascent yet vibrant digital industry. The reason why we call it nascent is that despite several decades of existence and investment, there is this overwhelming feeling of not having unearthed more than the tip of the iceberg. If you are still not convinced, just glance at the chart below.

No other industry today spawns so many innovative business models, many of which were launched from the comfort of a couch. The disruption to traditional industries due to these businesses is vast and almost immediate. Like most of you, we at Qwixpert have been repeatedly astonished by the progress made in thought and action by these businesses. “Digital” also dominates discussions in the corporate world, so much so that if a word cloud of all corporate utterances were to be created, “Digital” would probably take center place in the largest font size.

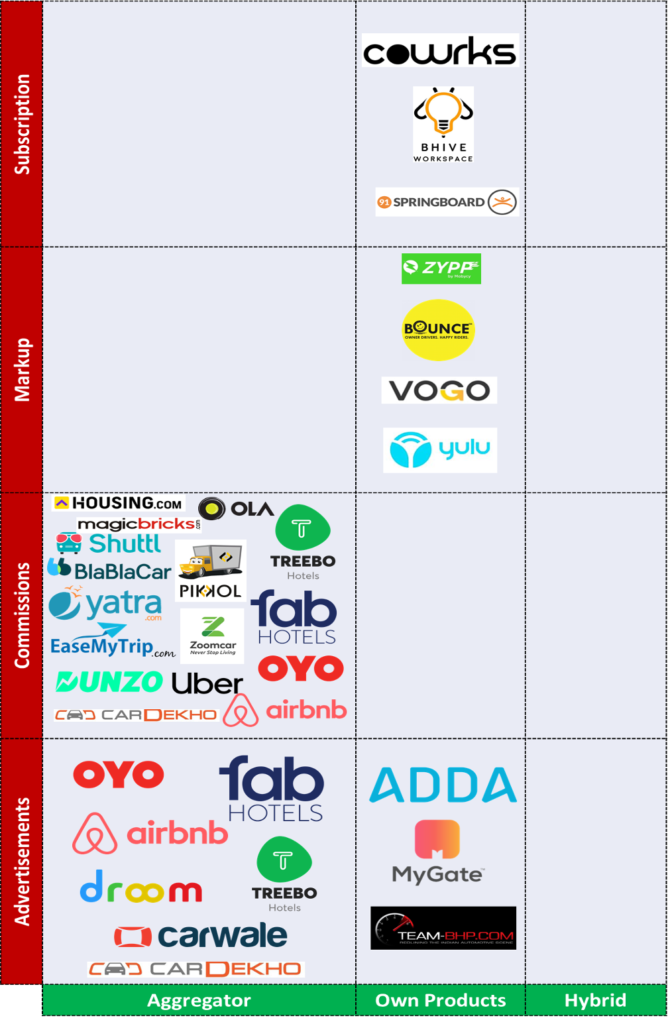

As “Digital” increasingly permeates our world, we have attempted to organize and structure it into a “Landscape.” We have limited our research to only Digital B2C businesses. The “Digital Landscape” is essentially a 2×2 matrix with “Business Model” and “Revenue Model” as its axes. These axes are defined as below

Business model – What is the product/ service? How is it offered to or experienced by the consumer?

Revenue model – How do they make money?

Business models can be classified into three kinds basis how consumers interact with the offerings on the digital platform

Aggregator – This is the often heard of marketplace model where a platform is provided for manufacturers/ service providers to interact and transact with potential customers. E.g., “Swiggy” is an aggregator platform for restaurants.

Own products – The digital platform is essentially a touchpoint to interact with customers for their products or services. E.g., Byju’s is a learning platform where consumers can access Byju’s own content.

Hybrid – Here, the digital platform is a touchpoint for own products and hosts products from other manufacturers/ service providers. The own products offered by the platform owner may or may not differ from products listed from other suppliers. E.g., Amazon has a hybrid business model where listings are of individual brands and Amazon’s private labels.

While the fine print on business contracts will reveal subtle differences in their revenue generation models, four principal types stand-out

Advertisements – Businesses pay for promotions and advertisements of their products/ brands on these platforms. E.g., Consumers are not charged for “Google searches” or “Facebook accounts,” while these companies generate the bulk of their revenues from ads and sponsored content.

Commissions – The platforms take a % of revenues or profits from every transaction that happens through it. E.g., Uber takes commissions on every ride booked on its app

Markup – The platforms purchase/ build/ manufacture products for a certain cost “X” and sell to consumers at “X-plus” through the digital platform. The key difference with the “Commissions” model is that the platform owns inventory, thereby running the risk of sitting on dead stock. E.g., BigBasket is an online food and grocery retailer which holds the inventory of the products sold on the platform

Subscriptions – Consumers pay a specific amount on a set frequency – Monthly, Quarterly, etc. – to access the platform. E.g., Netflix subscriptions to access their content

We have tried to “landscape” several industries into a 2X2 chart – Business Model X Revenue Model. While it is not an exhaustive list, a wide variety of companies operating in the following five industry sets are covered

Retail – General Retail, Food & Grocery, Durables, Fashion, and Home décor

Entertainment & Leisure – Social media, OTT, News, Gaming, Music, and Gifts

Productivity – Education, Recruitment, Financial Services, Books, and Open Source

Hospitality & Transportation – Automotive, Travel and Real Estate

Services – Health & wellness, Household help, Matrimony, and Virtual meetings

While companies do have hybrid revenue models, a separate category has not been carved out, but both are highlighted in case multiple revenue models are present. E.g., LinkedIn generates revenues through advertisements as well as subscriptions.

Retail – General Retail, Food & Grocery, Durables, Fashion, and Home décor

Entertainment & Leisure – Social media, OTT, News, Gaming, Music, and Gifts

Productivity – Education, Recruitment, Financial Services, and Open Source

Hospitality & Transportation – Automotive, Travel and Real Estate

Services – Health & wellness, Household help, Matrimony, and Virtual meetings

Key imperatives in the Indian Made Foreign Liquor industry today and trends driving themhttps://qwixpert.com/wp-content/uploads/2020/09/4.1_Industries_Alcoholic-beverages-1024x442-1.jpeg1024442qwixpertadminqwixpertadminhttps://secure.gravatar.com/avatar/392f1042eaff5c1f343a179d15026010?s=96&d=mm&r=g

Executive Summary

Per-capita alcohol consumption has seen an almost 3 fold increase since 2005 in India. A young population with ~50% above the legal drinking age, rising affluence, rapid urbanization and changing societal attitudes are driving this growth. However, alcohol consumption and IMFL penetration are not uniform across states indicating opportunities for growth of both economy and premium products. Mature markets are seeing increasing premiumization leading to expanding demand for Grain based ENA. Supply and cost pressures on Molasses based ENA due to the impetus on ethanol blending program, is leading to diversion of MENA production capacity to ethanol and a ~10% – 15% rise in ENA prices. This is expected to further augment GENA capacity leading to a ~186% growth between 2017 and 2022.

Supply security and sustenance of bottom-lines through cost reduction programs, alternate and innovative sourcing strategies are key challenges IMFL companies face in the short term. Economy segment strategy also becomes critical in the long run as cost pressures need to be balanced with potential opportunities in graduating country liquor consumers. While regulations prohibiting direct advertising pushed IMFL players to brand extensions, income generation potential from these businesses can be exploited to augment profits.

Alcohol consumption is rising as a social activity with increasing penetration and per capita intake

For many years, societies have discouraged individuals from alcohol consumption. Traditionally, alcohol consumers had largely fallen into one of two broad economic segments of the population – the elite, who enjoyed their drinks in the company of friends and family and the economically weak, who drowned their sorrows thanks to the intoxicating effects of liqour.

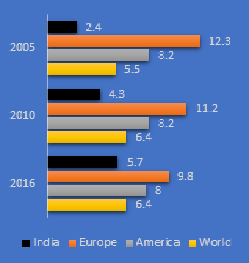

The widespread negative impression around drinking had kept per capita alcoholic consumption to as low as 2.4 until 2005, as against 12.3 for Europe and 8.2 for the USA (Ref. Chart 1) as per data from the World Health Organisation. A dramatic shift in behaviour seems to have occurred since then, across both India and Europe. While India saw a 2.5x growth in individual consumption, Europe has seen a ~20% contraction. Qwixpert’s analysis attributes the rapid increase in Indian consumption to three key factors.

Chart 1 – Per capita Alcohol consumption

Foremost among these is the increasing acceptance to drinking as a social activity. A recent study1 by IMRB-NFX, on behalf of National Restaurants Association of India, has found that 54% drink casually at social events. Respondents believed how celebrations have become incomplete without moderate alcohol. Easy access to information on the internet and awareness through social media have also contributed to the rise of social drinking.

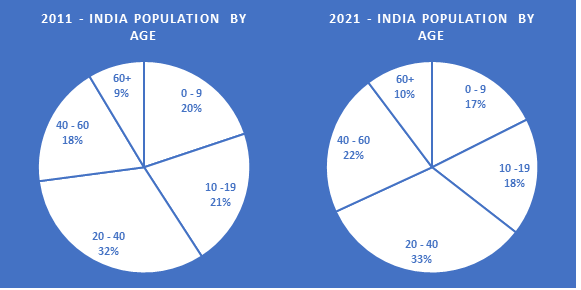

While consumption is increasing, so is the need to ensure responsible drinking. This trend is increasingly becoming prevalent among millennials (21 – 35 yrs. old)1 who are placing a great emphasis on consuming within limits. This has come as a boon for the “Bars and Pubs” segment who target the millennials and are growing at 23.5% annually3. This segment is expected to continue growing at a similar pace as India has a very young population with median age of 28 yrs2 and is likely to remain so in the near future.

Chart 2 – Split of India’s population by age – Median age 28 years

Chart 3 – Household composition

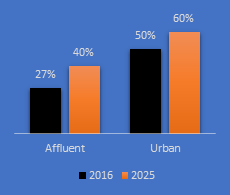

Favourable demographic mix with ~50% above the legal drinking age of 25 yrs has also contributed to increasing consumption. This mix is expected to become 56% in 2021 according to a report2 by MOSPI. This coupled with increasing urbanization and affluence (Refer Chart 3)4 will continue to positively impact liquor volumes through increased per capita consumption and enhanced penetration.

While a large majority still consume country liquor / indigenous drinks, state level differences in IMFL penetration opens up opportunities for customized strategies

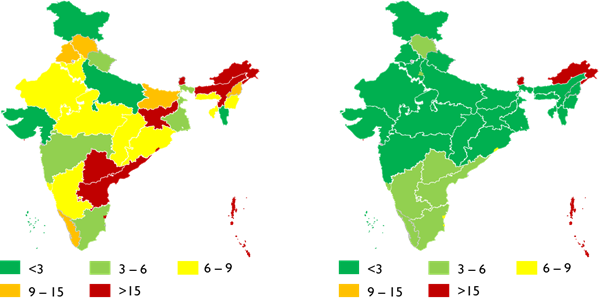

This consumption is heterogenous and according to a NSSO survey6, per capita consumption by state varies from 1.6 litres/ year in Mizoram to 57 litres/ year in Arunachal Pradesh. Most of this intake is in the form of country liquor, toddy and other indigenous drinks. Only, 7 states have >50% contribution of IMFL & Beer in overall liquor consumption. IMFL manufacturers need to design state level strategies to target increased revenue contribution from premium IMFL in these 7 states while driving migration to the “low-priced” economy segment from indigenous liquor in the remaining 22 states.

Chart 4 Per Capita Alcohol Consumption (Ltr/ Yr.) Chart 5 IMFL + Beer Per Capita Consumption (Ltr/ Yr.)

Premiumization is on the rise in Indian Made Foreign Liquor

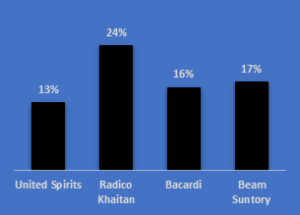

Chart 6 – Premium Alcohol sales growth (2018 vs 2015)

In mature markets with higher IMFL consumption, analysis of sales of various IMFL manufacturers suggest a growth in Premium alcohol volumes. Industry leaders have also seen this segment grow at 15%+ since 2015. Qwixpert research expects premiumization to continue further as industry leaders are re-orienting their resources to focus on premium IMFL sales while operating franchisees to ensure presence in the “economy” segment.

Capturing consumers with increasing disposable incomes migrating upwards to premium drinks and the millennial demand will be a key focus area for IMFL players. Industry experts believe this will lead to significant increase in malt spirit demand. With a significant portion of current demand serviced by imports, investments in new malt spirit plants are mushrooming as local cost-effective sources are being searched for by IMFL players.

Premiumization has also led to changes in the dynamics of ENA (Extra Neutral Alcohol) consumption in the industry. ENA contributes to 42.8% of most IMFL drinks. The industry has traditionally utilized molasses based ENA due to historical supply and cost advantages. Grain ENA, or ENA produced from grains unsuitable for human consumption, has been preferred by the best whiskey brands9 and IMFL companies are not to be left behind. While Pernod Ricard uses Grain ENA for 100% of its products, United Spirits’ Prestige & Above segments are 100% Grain based10

Ethanol Blending Program is diverting ENA capacity to ethanol; IMFL players are facing raw material supply and price pressures

Increasingly companies are shifting from MENA (Molasses based ENA) due to plateauing production of Molasses (Sugarcane) and diversion of MENA distilleries to ethanol production thanks to the Ethanol Blending Program (EBP). Oil Marketing Companies (OMCs) have been set a target of 10% ethanol blending by 2022, with a potential savings of Rs.12,000 Cr.11 on fuel imports between 2018 and 2022. An additional ~180 Cr. Litres of ethanol annually is required to satisfy the demands of the Oil & Gas industry.

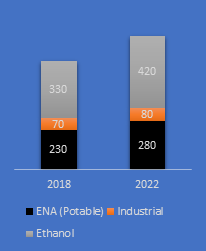

Chart 7 – Ethanol/ ENA demand (Cr. Litres)6

In order to fast track progress on the EBP initiative, in 2018, the government increased procurement price of ethanol from sugarcane by 25% from Rs. 47/litre to Rs. 59/litre. Further, B-heavy molasses-based ethanol is now 11% more expensive at Rs. 52/ ltr5.

ENA manufacturers are seen investing in converting distilleries from ENA to ethanol production to take advantage of the higher prices. This has led to an immediate contraction in ENA supply for the IMFL industry and ~10% – 15% increase in raw material procurement costs. ENA cost pressures have had an indirect impact on the push for premiumization from IMFL leaders. Contribution margins are decreasing in the price-sensitive economy segment driving focus on premium segments for sustaining profitability. A successful economy segment strategy will have to be built at a state level, considering current and projected market maturity for IMFL, production costs and business benefits of market coverage.

To guard against supply risks IMFL players must re-calibrate their ENA in-sourcing mix. Qwixpert analysis also indicates ENA procurement cost reduction opportunities existing in vendor consolidations and innovative sourcing contracts, to avoid spot purchases and secure ENA supply. Further, it is imperative that IMFL manufacturers focus on value engineering, alternate sourcing and innovative pricing techniques in packaging material for profitability.

Basis discussions with CXOs and experts in the industry, Qwixpert understands that GENA production is also burgeoning due to diversion of molasses to ethanol production. Increasing cost of regulatory compliance of discharge and complexity in managing effluent treatments plants for Molasses ENA distilleries, incremental revenue opportunity from DDGS (Distiller’s Dried Grains with Solubles) are also compelling IMFL players & ENA suppliers to set-up more GENA production units. Thanks to the abundance of “consumption unsuitable” grains, Qwixpert estimates the GENA capacity to grow by 186% from 88 Cr. ltrs. in 2017 to 252 cr. ltrs. in 2022. IMFL manufacturers investing in GENA capacities need to build detailed business cases to evaluate benefits of in-sourcing vs procurement.

Brand extensions: Necessity or opportunity?

The Cable television network (regulation) amendment bill12, which came into effect on 8th Sep 2000 has prohibited advertisement of alcoholic products on television. As a result, the companies have to limit promotional activity to point of sale or surrogate advertising using brand extensions like glasses, mineral water, music CDs etc. having identical brand names. Advertising Standards Council of India (ASCI) has set specific guidelines to qualify a brand extension product basis in-store availability of the product – at least 10% of the leading brand in the category the product competes (as measured in metro cities where the product is advertised) or turnover of the surrogate product or service at a minimum of ₹ 5 Cr. per annum nationally or ₹ 1 Cr. per annum per state where distribution has been established8. Further, these numbers have to be validated and certified by an independent organisation such as ACNielson or category specific industry association.

With tightening margins, alcohol manufacturers are no longer looking at brand extensions to keep the regulator off their backs but to make it a profitable business division. Products, such as water, soda and soft drinks, with synergies at similar points of sale as alcoholic beverages can beef up the bottom-lines with adequate strategic focus.

How digital and e-commerce are moving the restaurants beyond the physical real estate and how this is the path to recovery?https://qwixpert.com/wp-content/uploads/2023/07/Page-1_Image.jpg1379916qwixpertadminqwixpertadminhttps://secure.gravatar.com/avatar/392f1042eaff5c1f343a179d15026010?s=96&d=mm&r=g

Executive Summary

The coronavirus pandemic and the subsequent lockdown has crippled the foodservice industry. With operational constraints and an increase in customer apprehensions about ‘outside food’, the industry has to innovate to survive the crisis. In the recovery phase, the focus must be on sustaining business operations, operational solvency, and curating customer experiences.

In this article, Qwixpert explores some of the digital and on-ground interventions adopted by restaurants. They are offering safe dining experiences through contactless dining, social distancing at premises, and unmanned delivery kiosks. Innovations such as automation in food preparation, dark kitchens, and using online delivery channels can reduce cost burdens. Engaging with customers through social media can abate fears and influence them to eat out again. The industry is set to transform, and the changes will outlast the pandemic.

Background

The Foodservice industry is amongst the worst-hit sectors due to the Novel Coronavirus. Apart from being completely shut during the lockdown period, diner’s apprehension about consuming non-home cooked food and the fear of virus transmission in public spaces have continued to keep customer footfalls low even during the unlock phases. This drop in demand, coupled with a shortage of staff and disruptions in the supply chain, has led to an estimated $9 billion loss. Thus, bringing into question the industry’s sustenance in a post-COVID-19 world. As the foodservice industry opens up and slowly moves forward, we have analysed how their operating models have evolved to keep pace with the demands of the time.

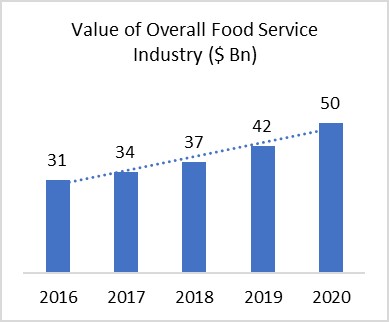

A $50 Billion industry with positively aligned macroeconomic indicators until the COVID-19 outbreak

The Indian market is valued at $50 Billion. The organised sector contributing to 30-35%, comprises of Casual Dining, Quick Service Restaurants, Bars and Pubs, and the Unorganised sector (65-70%) are made up of Dhabas, Roadside eateries, Sweet shops, and other smaller establishments.

The Foodservice industry has grown at ~13% CAGR (2016-2020). The growth was driven by increased frequency of eating out (6.6 times a month) and more spend on restaurants monthly (Average: Rs 2500 a month)

Online delivery, one of the most significant disruptions in the Food Service industry over the past decade, accounts for $1.54 Billion with a 3% share in the overall foodservice industry. It has been growing at 17.5% CAGR due to an increase in discretionary spending power, internet penetration, and a rise in the millennial population.

This period of strong growth has been interrupted by the pandemic. In the “Unlock” phases post the lockdown, restaurants were estimated to be operating at ~50% of their pre-COVID levels resulting in negative operating margins. The industry is expected to go through a long and slow recovery phase. New norms and practices have been implemented to meet Government stipulations and assuage customer concerns. We expand on the most visible and the not so visible ones below.

1. Providing a safe dining experience is the topmost priority

State SOP’s mandate thermal screening of all diners at the entrance, use of facemasks by employees and, in several instances, has capped seating capacity to 50% of pre-coronavirus levels. In several outlets, disposable cutlery and paper napkins are used, the tables and chairs are sanitised before and after use, and waiters use gloves and face shields while interacting with the customers. In June, the SOPs for restaurants in Chennai included food-bearers being mandated to wash hands every 30 minutes once.

Restaurants are redesigning their premise to make provisions for social distancing. Restaurants have spaced out the furniture and installed plastic curtains to create make-shift booths. As research has proved that the virus can transmit quickly in crowded indoor spaces, few restaurants are creatively using parking spaces to develop outdoor seating, offer drive-through take away or provide contactless drive-in restaurant service. In a recent survey conducted at Chennai, 61% of the respondents preferred to wait for a cure before venturing out for dinner; 73% preferred a drive-in option.

II. Adopting digital interventions to reduce contact with customers and dishes

Across the food preparation process, multiple people (chef, waiter, and other staff) touch the food increasing the chances of virus transmission. Automation in food preparation and delivery can reduce contact and abate fear – Robochef, a restaurant in Chennai, uses an automated kitchen where 600+ pre-programmed dishes can be prepared hygienically with 60% less workforce. Restaurants also use vending machines to offer contactless dine-in and takeaway experience. For instance, Daalchini has smart kiosks in Delhi that provide home-cooked food. The customer can discover the nearby Daalchini kiosks using an app, browse through the menu, and place orders digitally. They can visit the unmanned kiosk within half an hour to pick up their food.

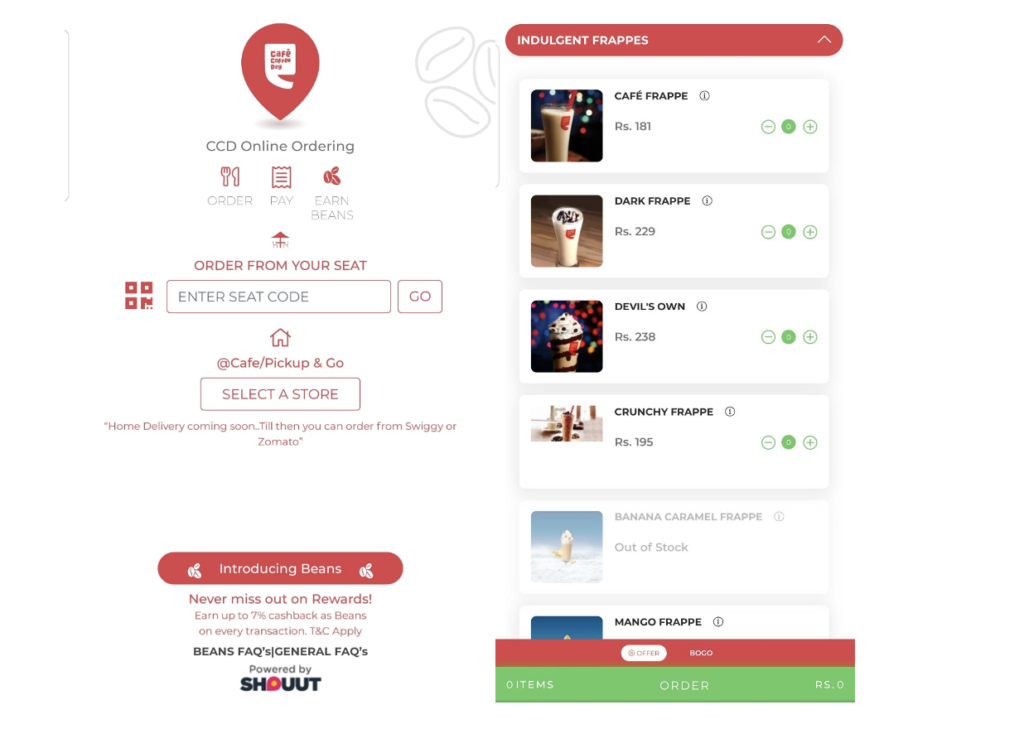

Restaurants have introduced QR code-based menus. Guests now scan the code to access the menu. Online ordering and payment practices are increasing at these times. Café coffee day has managed to open 60% of its stores post-lockdown by offering contactless dining through a web-based platform. Guests order from their seats by entering the seat code (pasted on the table), pay online, and get their food served at the table. The coffee chain wants to harness the data from this portal to understand the need of the customer and optimise a personalised experience for them.

III. Catering to online orders and developing lean operations is the new normal

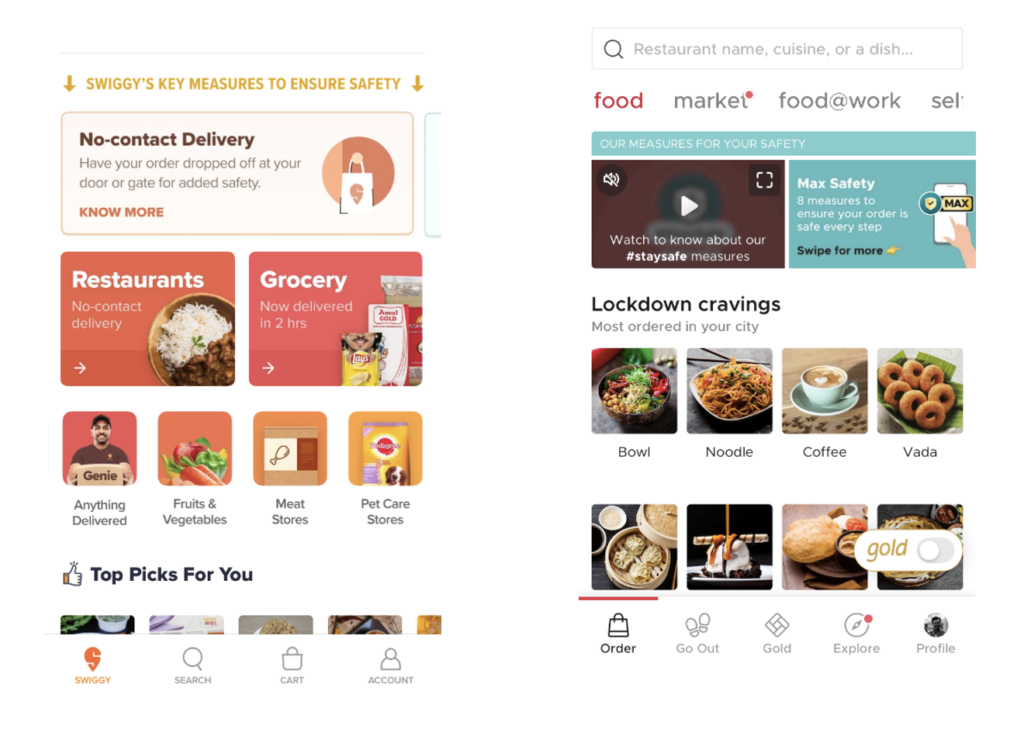

Restaurants may no longer be able to sustain without delivery capability. More and more customers are seeking to order online, and the reliance on delivery channels in the post-COVID world is bound to increase. Restaurants can separate menus – Delivery & Dine-in with a focus on improved packaging quality and have a separate order pick-up zone. Food delivery companies, as well as restaurants, will focus more on creating occasions for customers to order-in—Eg: Swiggy’s ads on delivering even a single piece of dessert to complete a meal. Pubs in the UK have started organizing online pub quizzes and allowing customers to order food and drinks to recreate the dine-in mood.

Restaurants are evolving their business model and setting up Dark kitchens that offer delivery only services and cater to the fast-growing consumer demand through food apps. Faasos, a pioneer in Indian cloud kitchens, was able to grow at 120% and expand to ~1,000 outlets in two years. Zomato and Swiggy have funded and developed ~1,600 cloud kitchens across India, which work on a revenue-sharing basis. These kitchens have been set up in partnership with traditional restaurants like Haldirams, Keventers, and Saravana Bhawan or launched under private brands like The Bowl Company.

While it is reported that Swiggy recently scaled down their dark kitchen business due to massive demand shock, we expect the cloud kitchen model to see more and more takers in the future. They are a safer alternative as customer contact is reduced, and social distancing can be practiced. During the lockdown, most restaurants have operated as Dark Kitchens and have continued even during the recovery phase that is a more efficient model. These kitchens reduce rental costs from ~12-20% to 6-9% of revenues.

IV. Investing in messaging around safety to dispel customer apprehensions and driving customer loyalty through social media campaigns

Marketing during pre-COVID times focused on attracting customers with offers, food choices, and the dining out experience, it has now pivoted more towards safe practice awareness as customer apprehension is at an all-time high. Questions abound on whether restaurants will continue to be looked at as social places for human interaction or functional ones to grab a quick meal in the event of necessity.

Personalised recommendations, loyalty programs, and discounts on food delivery apps along with tags such as ‘Max Safety’, ‘Best Safety’, and ‘Contactless Delivery’ are used to reassure customers who are looking to order-in.

Discounts and offers are still as high (if not more than pre-COVID). Restaurants that deregistered last year following a disagreement with these app-based delivery platforms are returning.

Restaurants are innovatively using social media to engage customers by offering online cooking classes with chefs, live streaming baking sessions, and organising wine delivery & tasting sessions over zoom calls.

V. Focusing on sanitation in procurement

Vegetable markets are being and will be eyed suspiciously by restaurants going forward. A preference for organised players who can be trusted to take social distancing measures, frequent sanitation of delivery trucks, contactless delivery, and online payments will rise. E-Procurement, using blockchain technology, is increasing transparency in the supply chain and makes it easier to enforce hygienic practices. The cleanliness of the ingredients is also a point of concern. Most state SOP’s for restaurants mandates the use of 50 PPM Chlorine to clean vegetables, dal, and rice. Zomato Hyperpure, Big Basket HoReCa, WayCool, and Dunzo are aggressively growing in this segment and cater to over ~10,000 partner restaurants.

Summary

In this race to recovery, organizations are leaving no stone unturned to rejuvenate operations, innovatively serve customers, and minimize the cost of operations. Sanitation of dining spaces, automation in food procurement, preparation and delivery, cloud kitchens, social media led long term customer engagement, and creating at-home dining occasions are where we are headed. As restaurants “reconnect” with their customers, from a safe distance, technology and efficiency are the pillars upon which recovery is being fashioned.